Black-Scholes is a model used to determine the theoretical value of a call or a put option in finance. A way that traders might use it is to buy an option priced under the Black-Scholes value and sell options priced higher than the calculated value. Larger firms might use the model to hedge, or attempt to eliminate risk, by buying and selling the underlying asset in just the right way. Here we solve the partial differential equation and calculate theoretical “fair” values for an option from one year to expiration to the expiration date.

Symbol definitions:

\(S(t)\) is the price of the underlying asset at time \(t\)

\(V(t,S)\) is the value of the option at time \(t\) and stock price \(S\)

\(K\) is the strike price of the option

\(r\) is the annualized risk-free interest rate

\(\sigma\) is the standard deviation of the stock’s returns

\(t\) is the time, in years, to expiration.

from devito import (Eq, Grid, TimeFunction, Operator, solve, Constant, SpaceDimension, configuration, centered)import matplotlib.pyplot as pltimport matplotlib as mplfrom sympy.stats import Normal, cdfimport numpy as npimport time as timer%matplotlib inlinempl.rc('font', size=14)configuration["log-level"] ='INFO'# Constants# The strike price of the optionK =100.0# The annualized risk free interest rater =0.12# The standard deviation of the stock's returnssigma =0.1# The S (price of the asset) range to processsmin =70smax =130# If you want to try some different problems, uncomment these lines# Example 2# K = 10.0# r = 0.1# sigma = 0.2# smin = 0.0# smax = 20.0# Example 3# K = 100.0# r = 0.05# sigma = 0.25# smin = 50.0# smax = 150.0# Amount of padding to process left/right (hidden from graphs)padding =10smin -= paddingsmax += padding# Extent calculationstmax =1.0dt0 =0.0005ds0 =1.0nt = (int)(tmax / dt0) +1ns =int((smax - smin) / ds0) +1shape = (ns, )origin = (smin, )spacing = (ds0, )extent =int(ds0 * (ns -1))print("dt,tmax,nt;", dt0, tmax, nt)print("shape; ", shape)print("origin; ", origin)print("spacing; ", spacing)print("extent; ", extent)

This differs from the regular Black Scholes PDE since our \(\frac{\partial}{\partial t} V(t,s)\) is negative. This is because instead of using a terminal condition, we are using an initial condition and solving backward in time.

Update equation

In our update equation, we solve for \(v.\text{forward} = v{\left(t + dt,s \right)}\).

We give this to Devito to solve for the next timestep of the problem. Our finite difference order of accuracy will be 4, meaning we will use two points off center to approximate the derivatives.

Initial and boundary conditions

The boundary conditions are the following:

Call option:

For very large S: \(V\left(t,S\right) \approx S\)

For very small S: \(V\left(t,S\right) \approx 0\)

Put option:

For very large S: \(V\left(t,S\right) \approx 0\)

For very small S: \(V\left(t,S\right) \approx K e^{-r(T-t)}\)

In this example we are solving for a call option. Because we have a set S range we are solving the problem in (smin to smax), we don’t need to worry about either of these boundary conditions. The initial condition will be:

\[V(t=T,S)=\max(S-K,0)\]

Where T is the time at expiration. For us this is flipped, so we set this condition at \(T = 0\).

When solving this problem, most approaches typically convert to the heat equation with a variable change of \(x=\ln S\), which gives a simpler PDE which is computationaly easier to solve. However, with the power of Devito, we can just solve the Black Scholes PDE directly.

Because this problem has non zero boundary conditions, we need to add a boundary condition on the right so that when the equation refers to out of bounds values it has a good approximation. Because the slope on the right is linear, a Neumann boundary condition is a good choice. Because our order of accuracy is 4, we need to implement the condition for two points past the right edge.

ASCII representation of what happens at the boundary:

| o v(t,smax+1)

| /

|/

o v(t,smax)

/|

/ |

v(t,smax-1) X |

/ | BC: constant slope for v when s >= smax

/ | need 2 points for a 4th order derivative

v(t,smax-2) X |

/ | slope = v(t,smax-1) - v(t,smax-2)

/ | v(t,smax) = v(t,smax-1) + slope

v(t,smax-2) X | v(t,smax+1) = v(t,smax) + slope

|

interior | boundary

(s < smax) smax (s >= smax)

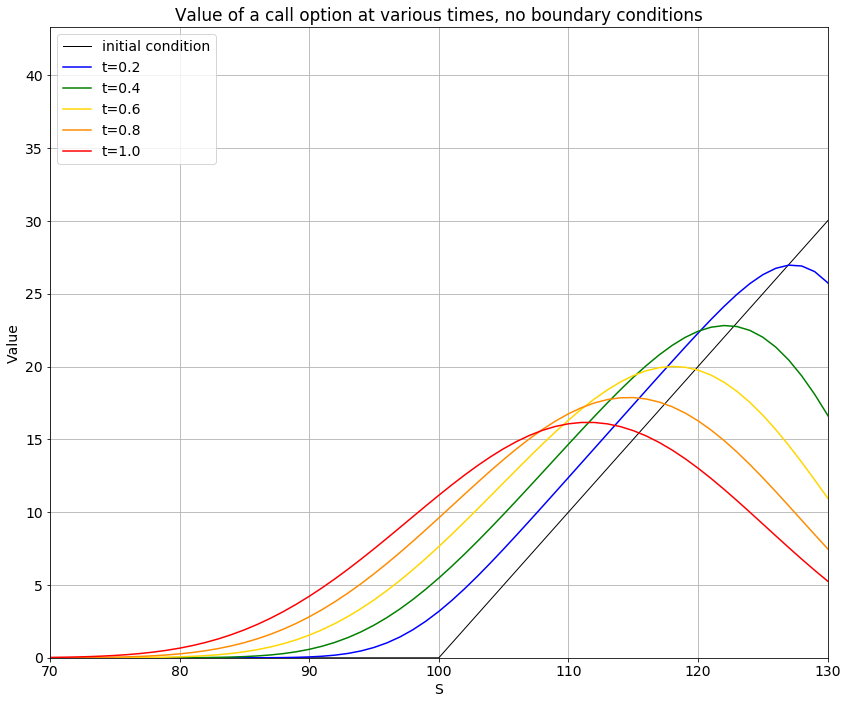

# NBVAL_IGNORE_OUTPUT# Get an appropriate ylimitslice_smax = v.data[:, int(smax-smin-padding)]ymax =max(slice_smax) +2# Plots = np.linspace(smin, smax, shape[0])plt.figure(figsize=(12, 10), facecolor='w')time = [1*nt//5, 2*nt//5, 3*nt//5, 4*nt//5, 5*nt//5-1]colors = ["blue", "green", "gold", "darkorange", "red"]# initial conditionsplt.plot(s, v_no_bc.data[0, :], '-', color="black", label='initial condition', linewidth=1)for i inrange(len(time)): plt.plot(s, v_no_bc.data[time[i], :], '-', color=colors[i], label='t='+str(time[i]*dt0), linewidth=1.5)plt.xlim([smin+padding, smax-padding])plt.ylim([0, ymax])plt.legend(loc=2)plt.grid(True)plt.xlabel("S")plt.ylabel("Value")plt.title("Value of a call option at various times, no boundary conditions")plt.tight_layout()

Here is what our plot looks like without boundary conditions. Because on the right side the derivatives try to read data that is not defined, the lines for the value of our option fall incorrectly towards zero.

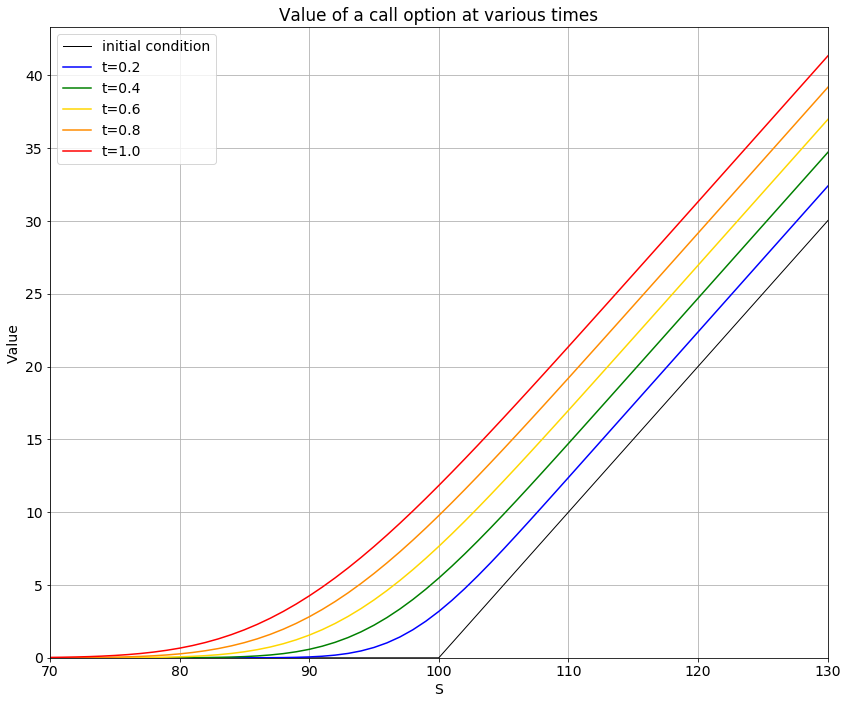

# NBVAL_IGNORE_OUTPUT# Get an appropriate ylimitslice_smax = v.data[:, int(smax-smin-padding)]ymax =max(slice_smax) +2# Plots = np.linspace(smin, smax, shape[0])plt.figure(figsize=(12, 10), facecolor='w')time = [1*nt//5, 2*nt//5, 3*nt//5, 4*nt//5, 5*nt//5-1]colors = ["blue", "green", "gold", "darkorange", "red"]# initial conditionsplt.plot(s, v.data[0, :], '-', color="black", label='initial condition', linewidth=1)for i inrange(len(time)): plt.plot(s, v.data[time[i], :], '-', color=colors[i], label='t='+str(time[i]*dt0), linewidth=1.5)plt.xlim([smin+padding, smax-padding])plt.ylim([0, ymax])plt.legend(loc=2)plt.grid(True)plt.xlabel("S")plt.ylabel("Value")plt.title("Value of a call option at various times")plt.tight_layout()

Plotting results

Above is a plot of our results. If the stock price is below the strike price at expiration, the option is worthless and thus the value is 0. At stock prices above the strike price, the value of the option is \(S - K\).

The red line is the value of the option 1 year from expiration. Orange is 0.8 years from expiration, yellow is 0.6 years from expiration, green is 0.4 years from expiration, and blue is 0.2 years from expiration. The black line is the initial condition (the value of the option at expiration).

Below we will plot the option value versus the stock value and the time to expiration as a surface.

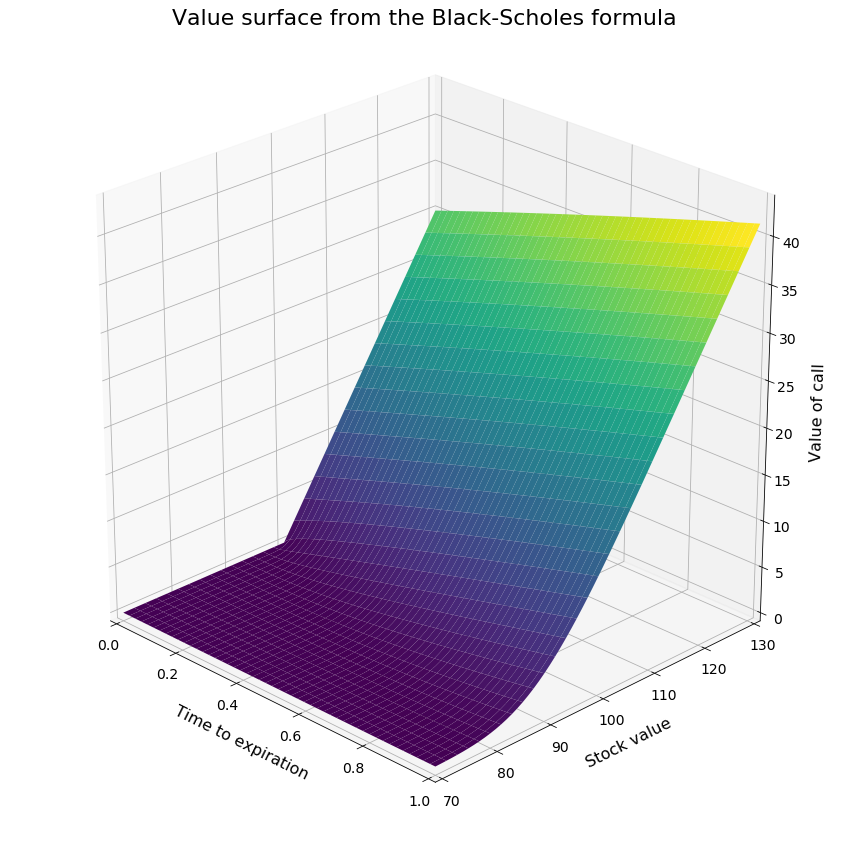

# NBVAL_IGNORE_OUTPUT# Trim the padding off smin and smaxtrim_data = v.data[:, padding:-padding]# Our axestt = np.linspace(0.0, dt0*(nt-1), nt)ss = np.linspace(smin+padding, smax-padding, shape[0]-padding*2)hf = plt.figure(figsize=(12, 12))ha = plt.axes(projection='3d')# 45 degree viewpointha.view_init(elev=25, azim=-45)ha.set_xlim3d([0.0, 1.0])ha.set_ylim3d([smin+padding, smax-padding])ha.set_zlim3d([0, ymax])ha.set_xlabel('Time to expiration', labelpad=12, fontsize=16)ha.set_ylabel('Stock value', labelpad=12, fontsize=16)ha.set_zlabel('Value of call', labelpad=12, fontsize=16)X, Y = np.meshgrid(tt, ss) # `plot_surface` expects `x` and `y` data to be 2Dha.plot_surface(X, Y, np.transpose(trim_data), cmap='viridis', edgecolor='none')hf.suptitle("Value surface from the Black-Scholes formula", fontsize=22)plt.tight_layout()plt.show()

Above is the option value plotted as a surface. Lighter colors represent higher value.

Using the derived formula for Black-Scholes at a point for comparison

Let’s take a look at the Black-Scholes derivation which gives us the value of a option at a point.

First some definitions. N(d) is the cumulative distribution function of the standard normal distribution.

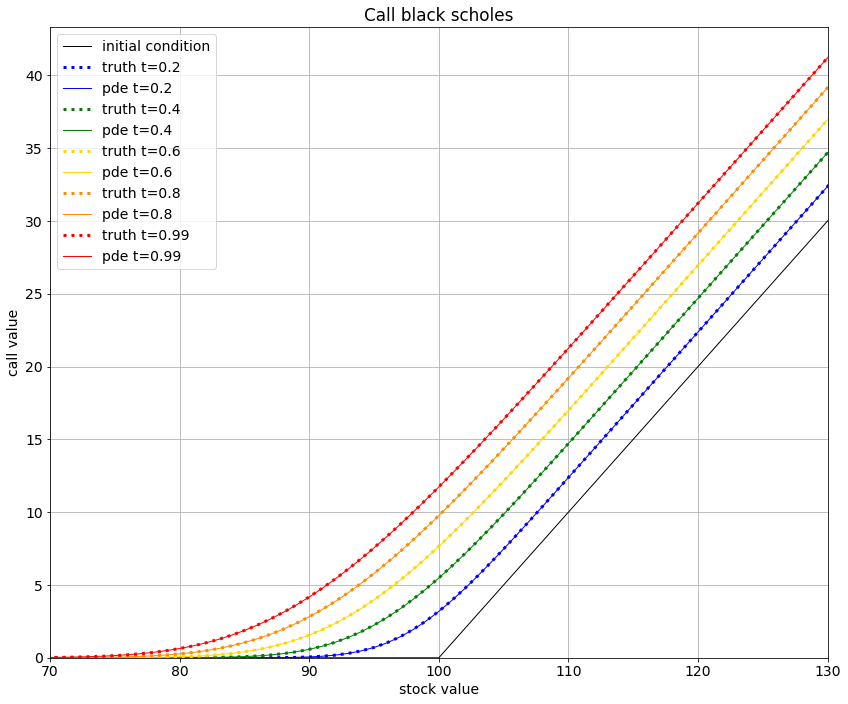

This formula is implemented below in the call_value_bs function. We run it on the same problem with 5 time values to compare our results from the formula to our results from solving the PDE with Devito.

The graph above shows the results from call_value_bs as a dotted line and the results from solving the PDE with devito as a solid line.

Comparing runtime of this function to Devito’s runtime is like comparing apples to oranges, but here is a quick comparison anyway. On a machine with a Ryzen 1800x with 8 cores, with 10000 time values ranging from 0.0 to 1.0, Devito takes 0.042 seconds to run the problem. With 5 time values between 0 and 1, running this function on the same problem takes about 4 seconds. This gives a reasonable idea of Devito’s performance in comparison to the alternative solution, i.e. stupid fast.

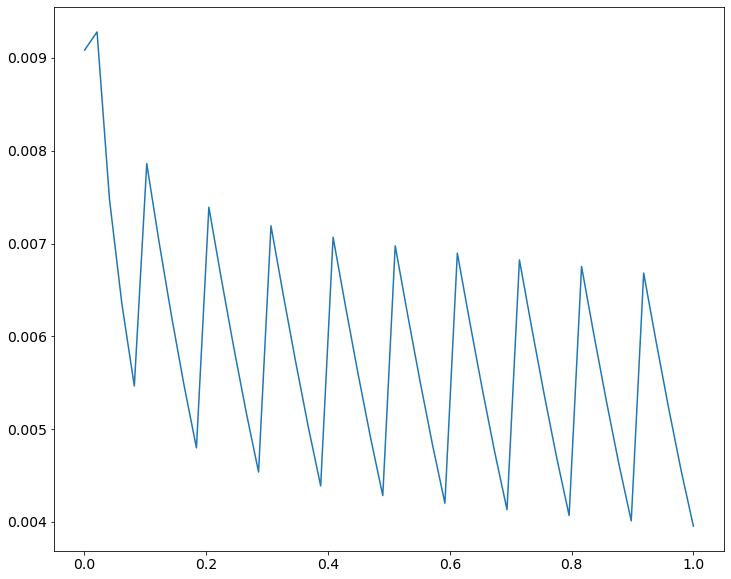

# NBVAL_IGNORE_OUTPUT# Plot the l2 norm of the formula and our solution over timet_range = np.linspace(dt0, 1.0, 50)x_range =range(padding, smax-smin-padding*2, 1)vals = []for t in t_range: l2 =0.0for x in x_range: truth = call_value_bs(x+smin, K, t, r, sigma) val = v.data[int(t*(nt-1)), x] l2 += (truth - val)**2 rms = np.sqrt(np.float64(l2 /len(x_range))) vals.append(rms)plt.figure(figsize=(12, 10))plt.plot(t_range, np.array(vals))

# NBVAL_IGNORE_OUTPUTnp.mean(vals)

0.00581731890853893

Above is a plot of the RMS error of our results from call_value_bs and Devito at a time t to expiration, which stays below 0.02 at all time values. The mean RMS error over all time is 0.0073, which is well below a tenth of a percent error.